WACC

DCF Workflow

Forecast Free Cash Flows

5-10 years of FCF based on operating assumptions.

Calculate Terminal Value

Gordon growth or exit multiple beyond projection.

Discount at WACC

PV each year's FCF, sum to enterprise value.

Adjust to Equity Value

Subtract net debt, divide by shares for per-share value.

Noble Desktop's Financial Analyst Training Program covers financial modeling, valuation, accounting, and Excel for finance.

Explore the concept of Weighted Average Cost of Capital (WACC), an important factor in performing Discounted Cash Flow Analysis for company valuation.

WACC or Weighted Average Cost of Capital is an important value used to perform Discounted Cash Flow Analysis to value the company.

So, what is WACC?

A company's capital funding is composed of two components: debt and equity.

WACC represents the investor's opportunity cost of taking on the risk of putting money into a company.

Let’s say 50% debt, 50% equity; If debtholders require a 10% return on their investment, and shareholders require a 20% return, then, on average, projects funded will have to return 15% to satisfy debt and equity holders – it’s WACC.

Here’s the formula for WACC. The cost of debt can refer to the before-tax cost of debt, which is the company’s cost of debt before taking taxes into account, or the after-tax cost of debt.

Calculating the cost of debt involves finding the average interest paid on all of a company’s debts. Or for DCF analysis often the current market 10-year bond yield applies.

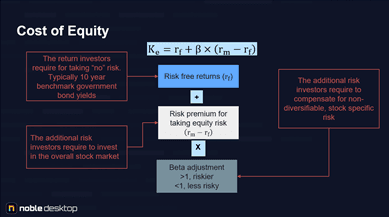

Calculating the cost of equity is a more complex process.