Journal Entry Examples

Common Journal Entries

Cash Sale

Debit Cash, Credit Revenue — straightforward exchange.

Credit Sale

Debit AR, Credit Revenue. Then Debit Cash, Credit AR when collected.

Inventory Purchase

Debit Inventory, Credit Cash or AP.

Depreciation

Debit Depreciation Expense, Credit Accumulated Depreciation.

Noble Desktop's Financial Analyst Training Program covers financial modeling, Excel for finance, accounting, and analytics for banking and investment careers.

Gain a deeper understanding of the accounting process by learning how to create journal entries, a crucial element in recording business transactions, and discover the rules and structure that govern this essential aspect of financial management.

A journal entry is used to record a business transaction in the accounting records of a business

A journal entry is usually recorded in the general ledger. The general ledger is then used to create financial statements for the business.

The logic behind a journal entry is to record every business transaction in at least two places (known as double-entry accounting).

For example, when you generate a sale for cash, this increases both the revenue account and the cash account. Or, if you buy goods on account, this increases both the accounts payable account and the inventory account.

The structure of a journal entry contains the following elements:

- A header line may include a journal entry number and entry date.

- The first column includes the account number and account name into which the entry is recorded. This field is indented if it is for the account being credited.

- The second column contains the debit amount to be entered.

- The third column contains the credit amount to be entered.

- A footer line may also include a brief description of the reason for the entry.

The structural rules of a journal entry are that there must be a minimum of two line items in the journal entry and that the total amount you enter in the debit column equals the total amount entered in the credit column.

A journal entry is usually printed and stored in a binder of accounting transactions, with backup materials attached that justify the entry. This information may be accessed by the external auditors as part of their year-end investigation of a company's financial statements and related systems.

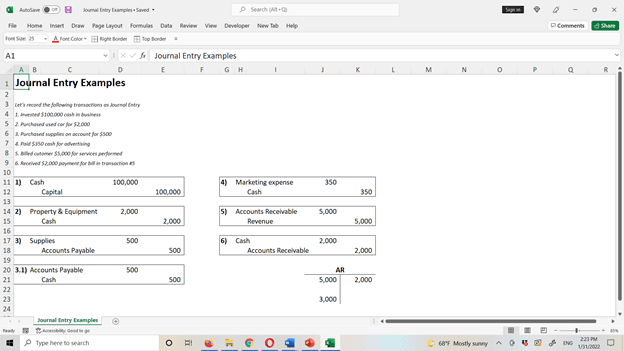

1) Cash and Capital will go up by $100,000.

2) We debit the Property and Equipment account. We will credit cash. Credit makes an asset go down, so it shows that cash goes down.

3) When we purchase on account – it means we are not using cash. Supplies being an asset will go up. As we are not doing it with cash, it means it does into accounts payable. Accounts payable is money owed by a business to its suppliers shown as a liability on a company's balance sheet. We have an asset going up and we have a liability going up.

3.1) When we pay the account payable liability off the journal entry will be reversed. Let’s just do 3.1 here just to show what will happen. AP will go away with the debit of $500. And we will pay out the cash that we owe to the suppliers with the credit of $500.

4) Advertisement expense will be debited for $350. And we paid for this expense with cash, so we will credit cash for $350.

5) We only billed customers, which means we are not receiving the actual payment yet. So, there’s no cash in this transaction. We do have an asset though because the clients owe us money – that would be account receivable. Accounts receivable is the balance of money due to a company for goods or services delivered or used but not yet paid for by customers. So, AR will go up by $5,000. To balance this transaction out we have equity in the form of revenue for the services delivered to the customer. So, the service revenue will be credited for $5,000.

6) Clients didn’t pay the full amount of $5,000 yet, but they paid $2,000. It happens, sometimes the bill is paid off in tranches. We know that we are receiving cash, which means we’ll debit cash for $2,000. The tendency is to want to credit revenue now, but in fact, we’ve already recognized the revenue in transaction #5. So, if we credit the revenue again, we are going to double-count it, and we’ll have $5,000 and $2,000 revenue in our income statement when we only want $5,000, which we’ve already recorded. So, what’s happening, the AR is actually going to go down, and the amount that the clients owe us is actually going to go down. So, we credit AR for $2,000.

If we draw a little T-account for AR. When we bill the client, they owe us $5,000. And then we credited AR in transaction #6 for $2,000. So, the balance that the client owes us now is $3,000.

Journal entries and attached documentation should be retained for a number of years, at least until there is no longer a need to have the financial statements of a business audit. The minimum duration period for journal entries should be included in the corporate archiving policy